Moving from California with Startup Equity

TL;DR: If you were granted equity compensation while a resident of California, you may still owe California tax on that equity even after you move to another state. The type of equity you have (i.e. ISOs, NSOs, or RSUs), as well as the amount of time you spent as a non-resident of California, are important factors when determining if and how much you will have to pay in California taxes on your equity after you move. California will tax the spread between the grant price and exercise fair market value (FMV) to the extent you were working for a company while a resident of California. In general, the longer you live outside of California before you exercise, the less your equity will be subject to California tax as long as you stay with the company.

As a startup founder or employee, you may be wondering if you can save money on taxes by moving from a high-tax state like California to a lower-income-tax state or no-income-tax state or territory [0]. Let’s discuss the tax scenarios around leaving California based on the different states you might move to, the different types of equity you might have, and when you might choose to exercise your options.

[0] Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington and Wyoming have no income tax. Note that if you leave the country, 100% of your income will still be taxable to the United States and the state where you were granted your equity.

Non-Qualified Stock Options (NSOs)

For NSOs, if you are granted equity while a resident of California and then move to a different state, where you then become a resident and exercise your options, California will tax the NSO income based on the total amount of time you spent as a California resident from the grant date (the date you were granted your equity) to the tax date (the date you exercised or purchased your options). [1]

For example, let’s assume you were a California resident and you have 5,000 NSOs, with:

- Exercise price of $1

- FMV price of $11 (at all relevant times following the grant)

All granted on January 1, 2020. You move to Texas (a state with no income tax) on June 30, 2020.

The scenarios below show how much your equity compensation would be subject to California tax if you exercised all of the shares in 2020, 2021, or 2022.

Moving from California to Texas with NSOs

[1] % of the time spent in California = (Date moved to Texas - Grant Date) / (Exercise Date - Grant Date)

49.59% = (181 days) / (365 days)

When you exercise your NSOs, remember you accrue ordinary income on the difference between the grant price and the fair market value (FMV), determined based on a 409a valuation, of the shares at the moment of exercise multiplied by the number of shares exercised. This income is partially subject to California taxes in the above scenarios.

If you want to move out of California, you’ll most likely owe California taxes on your equity (assuming that’s where it was granted). But as you can see above, the longer you live outside of California before you exercise, the less tax you’ll owe to California. So as a rule of thumb, residing outside of California before exercising for longer minimizes your overall tax burden. An important caveat, this is only the case if you stay with the company. If a taxpayer leaves the state AND leaves the job, technically no services were performed out of state as part of equity calculation. [1]

Selling your NSOs

What about when you sell your equity? When you sell your NSOs, the spread between the current FMV/409a valuation and exercise price is considered a capital gain or loss.

One upside to moving out of California comes from saving on taxes you’ll owe when you sell your exercised options (also known as shares). Namely, if you move out of California to a no-income-tax state and sell your exercised NSOs, none of the resulting gain will be subject to California state income tax!

Moving from California to NY with NSOs

Let's take the same Scenario #1 above but instead of moving to a state with no income tax like Texas, you move to a state that has income tax such as New York. When you exercise your NSOs, 100% of the income from exercising will be taxable to your new state of residence, New York. You will pay tax on 100% of the total income ($50,000) to New York state, but you will also have to pay tax on the income subject to California taxes ($24,795). Because you were essentially double-taxed on the income, you should be able to get a credit [2] against your New York taxes based on the amount of tax you paid to California. Note: New York City has its own city tax. You won’t be able to take a credit against New York City tax for the double-taxed equity income. [2]

[2] A single filer in California would pay $315 on $24,795 of California-sourced income.

What if I move to California from out of state?

Alternatively, if you were granted NSOs while a resident of another state and then moved to California and exercised there, 100% of the income and subsequently the capital gains when you sell your options would be subject to California taxes. Similar to the above scenario, if you paid any tax to another state when you exercise, you generally will also be able to take a credit against your total California tax based on the amount of tax you paid to the other state.

Incentive Stock Options (ISOs)

As a reminder, when you exercise ISOs, the spread between the grant price and the FMV at exercise multiplied by the number of shares exercised is considered an alternative minimum tax (AMT) adjustment for both California and Federal income tax purposes, not ordinary income. This section discusses potential changes to the amount of California AMT owing as a result of ceasing to be a California resident, the amount of Federal AMT will not change. This AMT adjustment is included in the AMT calculation and depending on your income and deductions for the year, may generate AMT you will owe.

For ISOs, if you were not a resident of California when you exercised, you will need to determine the amount of AMT adjustment based on the time you spent as a California resident from the grant date to the exercise date. Based on the amount of AMT adjustment, you may or may not have to file taxes in California when you exercise. [1]

For example, in the scenarios below, assume you were a California resident and granted 20,000 ISOs with:

- Exercise price of $1

- FMV price of $6 (at all relevant times following the grant)

All granted on January 1, 2020. You move to Texas (a state with no income tax) on June 30, 2020.

Each scenario shows the AMT adjustment you would need to make to determine if you owe California taxes, assuming you exercised all of the shares in 2020, 2021, or 2022.

Same as in the NSO example above, the longer you live outside of California, the smaller the amount of AMT adjustment that will be subject to California taxes.

If you later sell the exercised stock in a qualifying disposition (at least two years from the grant date and one year from the exercise date), California will not tax the capital gain. Additionally, you may be able to take an AMT credit to reduce any California-sourced income you had in that year.

If you later sell the exercised stock in a disqualified disposition (sooner than two years from the grant date and one year from the exercise date), California will tax the spread between the FMV at exercise and the exercise price as ordinary income. In the example above, assuming Scenario #1 (earliest exercise date) and a disqualifying sale, you would need to pay ordinary income tax on $49,589 to California. Any capital gains associated with the sale (if the stock was sold for any amount above the exercise price) would not be taxable to California. Similar to the NSO examples above, you could potentially be eligible for a credit against your new resident state tax based on the amount of California tax you paid.

If you were granted ISOs while a resident of another state and then moved to California where you exercised, 100% of the AMT adjustment and capital gains when you sell would be subject to California tax.

Restricted Stock Units (RSUs)

The unique thing about RSUs is that they vest depending on a set schedule over time (generally monthly or quarterly) with no concept of exercising.

Note that there are also “two tier RSUs” AKA “double triggered RSUs” which are only taxed following both time-based vesting and satisfaction of a liquidity event condition.

When the shares vest, the FMV of the stock multiplied by the number of shares vesting is the amount of ordinary income you are taxed on.

For RSUs, if you were granted the RSUs while a resident of California but vested them after moving out of state, California will tax the wage income as each tranche of your RSUs vests based on the portion of the time you spent in California from the grant date to each vest date. [1]

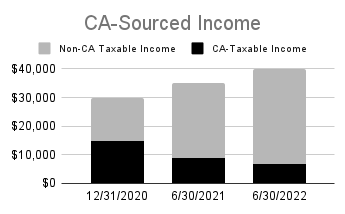

For example, in the scenarios below, assume you were a California resident and were granted 3,000 RSUs on January 1, 2020 where you vest into 1,000 shares starting 12/31/2020 and 1,000 subsequent shares on 12/31/2021, and 12/31/2022.

You move to Texas (a state with no income tax) on June 30, 2020. The scenarios below show how much your equity compensation would be subject to California tax, the longer you stay outside of California.

As you can see, just as with ISOs and NSOs, for RSUs, the longer you stay outside of California, the less income you have to pay taxes on to California. By the end of your third vest, you only end up being taxed on less than a third of your total vested income to California (total wage income of $105,000 and California-sourced income of $30,167).

Similar to the NSO and ISO scenarios, you don’t owe any capital gains tax to California if you sell shares issued upon vesting of RSUs when you are no longer a California tax resident.

In short, the longer you live outside of California, the less you have to pay to California in taxes as long as you stay with the company. A big upside is the savings on capital gains tax. Namely, if you sell your exercised options or previously vested and held shares subject to RSUs outside of California, you won't have to pay tax to California on the gain of the sale . But the specific amount of savings depends on the type of equity you have and the price at exercise. For more information or advice on your individual circumstance, contact your financial advisor.

Summary Table

FAQ

Q: If I move from California to Texas and exercise my options, will I be subject to California tax?

A: Partially. You will not owe taxes on the capital gains when you sell your stock. However, when you exercise, a portion of either the ordinary income or AMT adjustment will be subject to California taxes based on the total time spent in California from the grant date to the exercise date.

Q: If I move from California to another state such as New York and exercise my options, will I be double-taxed on the income portion of my equity?

A: The entirety of the income portion of your equity exercise will be taxable to your state of residence. (Let's assume New York). In addition, you will realize income based on the amount of time you spent in California (see above examples) and pay tax on that amount. Most states, New York included, allow you to take a credit for taxes paid to another state on income that is already taxed to that state. So initially you will be double-taxed, but you may be able to offset some or all of that additional California tax by a reduction of your residency state taxes.

Q: I may have a liquidity event this year, what happens if I move out of California before the liquidity event?

A: If you have already exercised your equity and established residency in another state before the liquidity event, you won't have to pay any California taxes on the proceeds from the liquidity event. If however, you still need to exercise your stock options before the liquidity event, part of your income piece from exercise will still be subject to California income tax.

Glossary of Terms

AMT Deferral Amount = (exercise price - grant price) x number of shares exercised

Wage Income - Any regular wage you are paid by an employer like an hourly wage or a salary

AMT Credit - A dollar-for-dollar reduction of any future ordinary taxes based on the amount of AMT you have paid in previous years.

Citations

[1] State of California Franchise Tax Board - Equity-Based Compensation Guidelines - Publication 1004

[2] Credits for New York State residents - NY State department of taxation and finance